Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

Decreasing cash flows are a telltale sign that company might be headed for distress. However, negative impacts on cash flow are the result of various factors - decreasing margins, slower sales, increasing costs along with many other reasons which will cause cash flows to decrease. If you are finding your bank balance dwindling or your line of credit rising without understanding the cause, then you have a problem. Get focused and start researching the reasons.

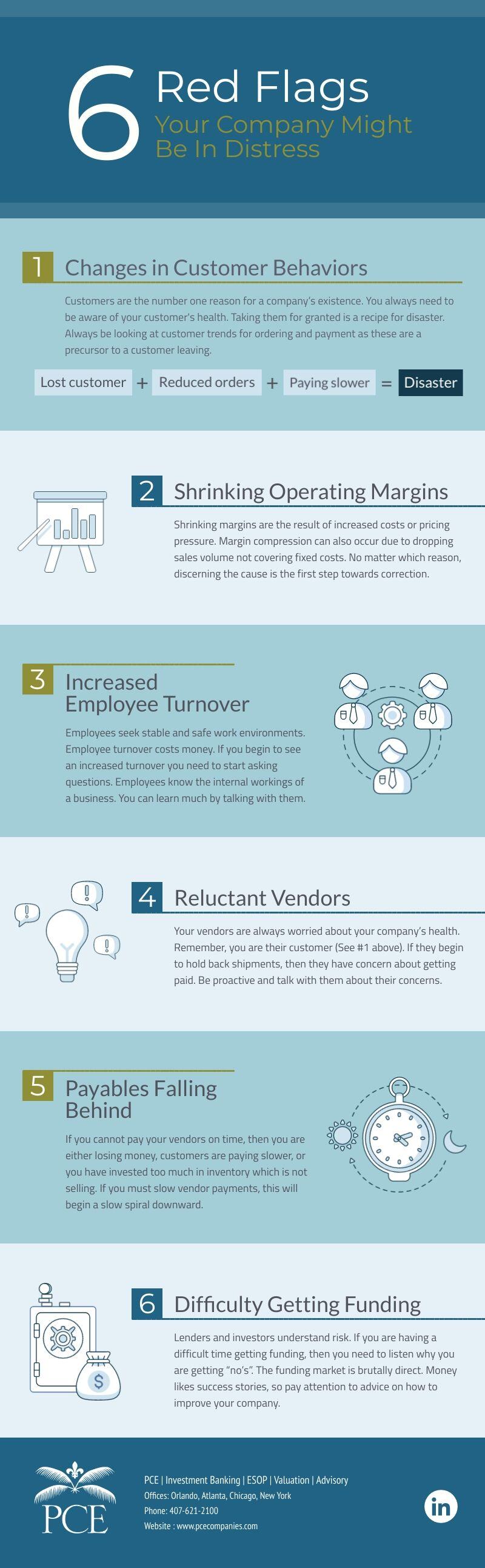

Customers are the number one reason for a company’s existence. You always need to be aware of your customer’s health. Taking them for granted is a recipe for disaster. Always be looking at customer trends for ordering and payment as these are a precursor to a customer leaving.

Shrinking margins are the result of increased costs or pricing pressure. Margin compression can also occur due to dropping sales volume not covering fixed costs. No matter which reason, discerning the cause is the first step towards correction.

Employees seek stable and safe work environments. Employee turnover costs money. If you begin to see an increased turnover you need to start asking questions. Employees know the internal workings of a business. You can learn a lot by talking with them.

Your vendors are always worried about your company’s health. Remember, you are their customer (See #1 above). If they begin to hold back shipments, then they have concern about getting paid. Be proactive and talk with them about their concerns.

If you cannot pay your vendors on time, then your either losing money, your customers are paying slower, or you have invested too much in inventory which is not selling. If you must slow vendor payments, this will begin a slow spiral downward.

Lenders and investors understand risk. If you are having a difficult time getting funding, then you need to listen why you are getting “no’s”. The funding market is brutally direct. Money likes success stories, so pay attention to advice on how to improve your company.

If you have comments or questions about this article, or would like more information on this subject matter, please contact us.