Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

.png?width=728&name=Download-PDF%20(1).png)

Visit our Exit Planning Library to find additional resources to help guide you through the exit planning process.

You’ve spent years successfully growing your company, and now it’s time to reap the rewards of the value you created. There are many options available to extract value, but this eBook will focus solely on selling.

As you begin to contemplate selling your building products business, it is essential to understand what buyers are looking for. Now is the time to make your business more marketable by addressing areas that need improvement. Whether you are ready to sell now or just interested in preparing for the future, the following pages detail key processes that will strengthen your business and its marketability.

Don’t put all your eggs in one basket—this idiom applies to revenue drivers too. Having a diverse range of clients and a strategic geographic presence minimizes the impact of any one client’s decision to cease operations or choose another supplier. The more diversified your company’s revenue stream, the more valuable that revenue stream is to a potential buyer. Key client relationships are fine; just make sure no one client represents more than 10 percent of your yearly revenue. If one client does, shift your focus to growing revenue from other clients in order to limit the amount client concentration.

Successful companies recognize the importance of adapting to the needs of buyers. Creating demand for a product drives revenues year after year. As market demands change, you will need to prove that your company is adaptable to consumer demands and market preferences. This ability to adapt will make your business even more attractive and valuable.

One key challenge facing companies in the building products industry is the need to enhance each product with eco-friendly or smart capabilities. An example of a company meeting this challenge is 3M’s introduction of its innovative granular product, which eliminates smog when it’s applied to roofing shingles and activated by the sun.1 An earlier example of an innovative product was the introduction of drywall to the marketplace by U.S. Gypsum Company. The ability to acclimate to changing demands is vital.

Establishing solid relationships with multiple vendors and suppliers is key to obtaining the resources necessary to produce your unique product(s). Having several sources at your disposal to obtain raw materials and/or finished goods will drive up the value of your company. Demonstrating relationships with multiple suppliers assures a potential buyer that your company is not supplier-dependent.

Since there is a risk (profitability impact) to holding inventory, working with multiple suppliers generally indicates that resources and materials are readily available to you, which indicates that you took the necessary steps to manage costs. Having multiple relationships will add value to your company and pique the interests of buyers. Your potential buyers will quickly recognize that fundamental materials and/or goods can be sourced without having to incur significant expenses or being locked into a single-supplier agreement.

Potential buyers have their own supplier relationships that they’ve fine-tuned in order to create efficiencies in their businesses; however, by showing that you have done the same work while simultaneously growing your company will result in a much stronger offer. Make sure your contracts are well-documented and assignable in the event of a sale. The contracts in place should reflect your purchasing power with respect to the raw materials.

Keep detailed records of your production process; ensure these records accurately reflect expenses, indicating that your gross profit margin is sustainable and stable. Demonstrating that you can maintain gross profit margins increases the value of your company—and the value of any deal.

As an added bonus, documentation showing that you’ve optimized your cost structure in order to achieve economies of scale will demonstrate that you’ve been successful in passing on cost increases resulting from external factors, such as tariffs, oil prices, natural disasters, and other events outside your control, in the form of price increases—without negatively impacting profitability.

The key to your company’s success is building a skilled workforce—and one that works as a team in order to meet shared goals and objectives. Having a highly tenured staff and secondary level of management in place demonstrates your company’s ability to remain profitable without your leadership. We all want to be irreplaceable, but here you need to show the company can thrive in your absence. Retaining and training capable employees is integral to driving additional value to your business.

Environmental compliance is a crucial consideration when selling your building products company. Having all documentation, whether it’s a Phase 1 or EPA report, is essential to show that your company’s operations have not negatively impacted the local or global ecosystem. Keep detailed records that confirm the proper disposal of any materials, which may pose a risk to the environment. If your company is found to be harmful to the environment, your brand reputation takes the hit, resulting in a decrease in not only the value of your company but also the chances of finding a buyer.

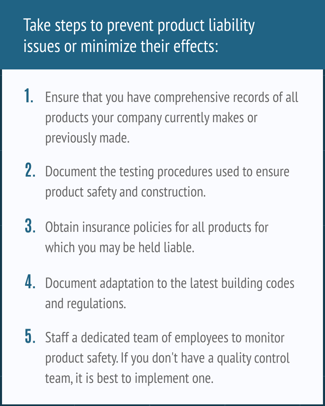

One of the most crucial elements of your building products company is product liability. Take asbestos, for example. It was previously identified as being safe, but we know today of its deadly consequences. While most governments have become better at identifying potentially harmful substances, innovation has been happening so quickly that latent issues could arise from a host of products. It’s sometimes simply unknown territory.

In addition to potentially harmful substances, product failure in the building products industry has vast repercussions. In London, highly flammable exterior cladding, which was not designed for high-rise buildings, has been linked to the rapid spread of fire in those structures. Approved uses of cladding exist; however, the improper use of this material can result in a product liability claim against the company.2,3

Before any sale can be finalized, you will need to indemnify the buyer from any potential claims that may arise or result from your time as owner of the company. Protect your future proceeds—make sure you can prove you were not negligent with respect to potential claims, by following the steps above. Also take into consideration that a buyer will not be willing to pay maximum value for a company that does not have an exemplary documentation process. If you can’t presently produce the above list of items, start implementing these processes now.

Obtaining the maximum value for your business is just as much about timing as it is about addressing all the issues outlined to this point. The company you have built over the years is interdependent on the overall health of both the market and the construction industry. Valuations of building products companies are diminished when the construction market is in a downward trend, as evidenced during the great recession. As the construction market recovered, pent-up demand for construction services positively affected the marketability of building products companies. When the market is good, you will find a buyer willing to pay the proper market value of the company. To ensure that you obtain the maximum value of your business, spend time addressing the items listed in this article. Completing a little paperwork and implementing a few processes can yield a sizable profit for you.

Selling your business is a life-changing decision that must be made with care. It’s never too early to start preparing for your succession. Some of our most successful transitions started with conversations five years before the actual sale. We’re happy to discuss your particular business and provide value-adding strategies that you can implement now that will increase your value later. Contact us today to get more information about how we can help.

To supplement this article, please refer to our Guide to Selling Your Business.

PCE has a team of credentialed investment bankers and valuation experts available to help you. Whatever you wish to accomplish, our team can define, analyze and present solutions that allow you to take the next step.

Visit our Exit Planning Library to find additional resources to help guide you through the exit planning process.