Industry Trends

Largest Transactions Closed

- Target

- Buyer

- Value($mm)

Last updated:

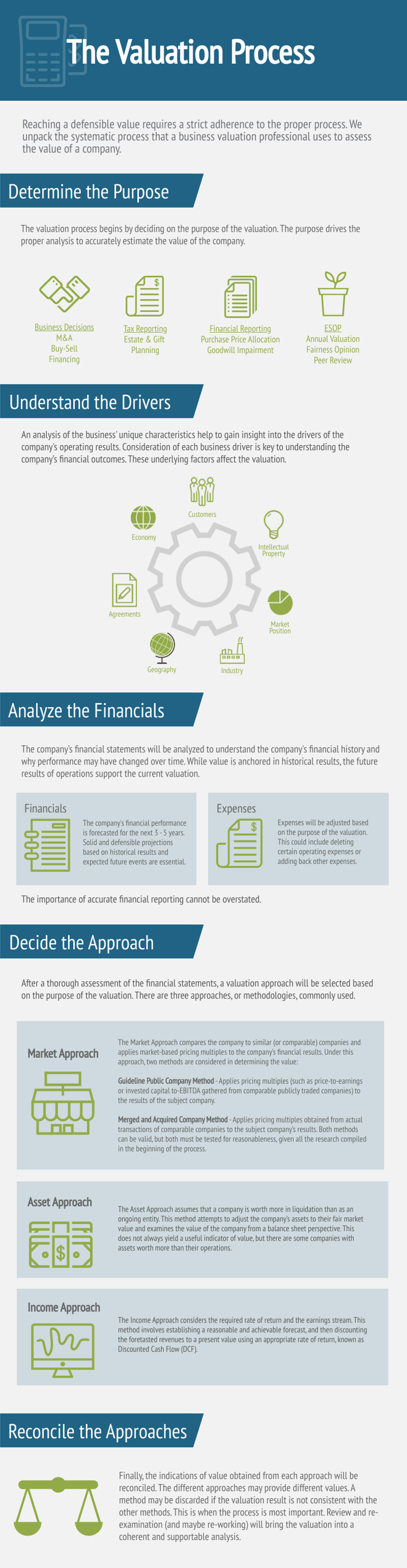

Reaching a defensible value requires a strict adherence to the proper process. We unpack the systematic process that a business valuation professional uses to assess the value of a company.

The valuation process begins by deciding on the purpose of the valuation. The purpose drives the proper analysis to accurately estimate the value of the company.

An analysis of the business' unique characteristics help to gain insight into the drivers of the company's operating results. Consideration of each business driver is key to understanding the company’s financial outcomes. These underlying factors affect the valuation:

The company’s financial statements will be analyzed to understand the company's financial history and why performance may have changed over time. While value is anchored in historical results, the future results of operations support the current valuation.

The company's financial performance is forecasted for the next 3 - 5 years. Solid and defensible projections based on historical results and expected future events are essential.

Expenses will be adjusted based on the purpose of the valuation. This could include deleting certain operating expenses or adding back other expenses.

The importance of accurate financial reporting cannot be overstated.

After a thorough assessment of the financial statements, a valuation approach will be selected based on the purpose of the valuation. There are three approaches, or methodologies, commonly used in valuing a company.

The Market Approach compares the company to similar (or comparable) companies and applies market-based pricing multiples to the company’s financial results. Under this approach, two methods are considered in determining the value:

The Asset Approach assumes that a company is worth more in liquidation than as an ongoing entity. This method attempts to adjust the company’s assets to their fair market value and examines the value of the company from a balance sheet perspective. This does not always yield a useful indicator of value, but there are some companies with assets worth more than their operations.

The Income Approach considers the required rate of return and the earnings stream. This method involves establishing a reasonable and achievable forecast, and then discounting the foretasted revenues to a present value using an appropriate rate of return, known as Discounted Cash Flow (DCF).

Finally, the indications of value obtained from each approach will be reconciled. The different approaches may provide different values. A method may be discarded if the valuation result is not consistent with the other methods. This is when the process is most important. Review and re-examination (and maybe re-working) will bring the valuation into a coherent and supportable analysis.